Heartwarming Provision For Doubtful Debts Is An Expense 2019 Profit And Loss Form

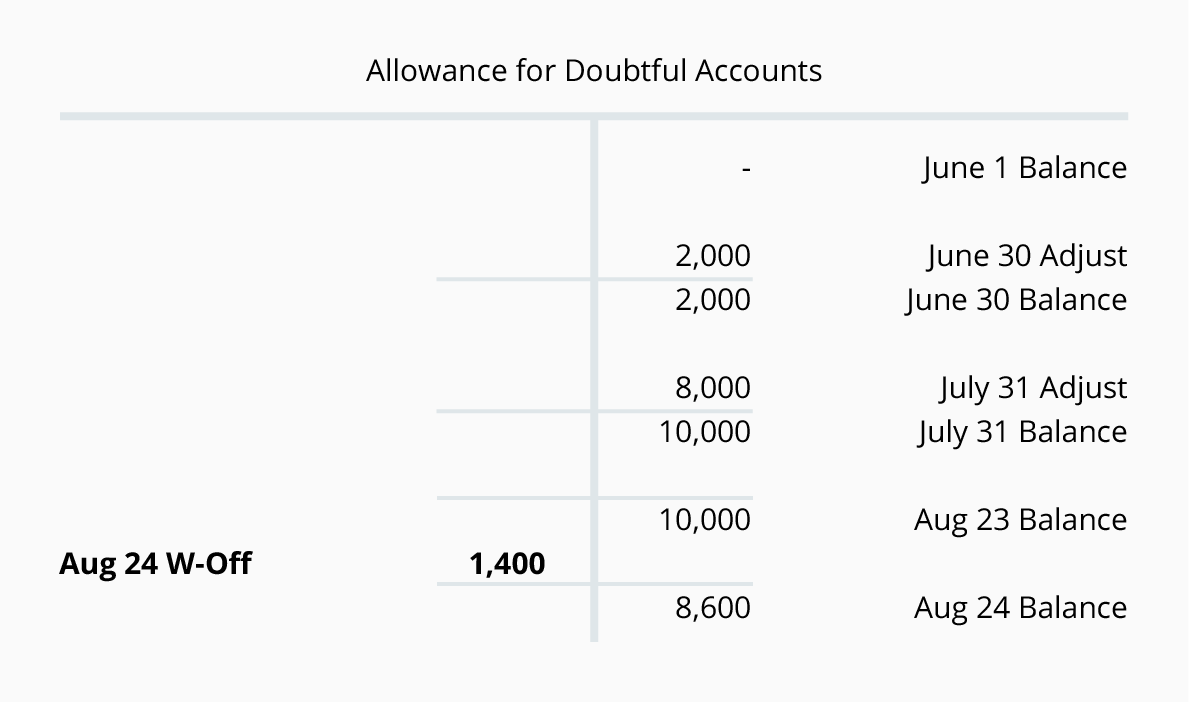

Writing Off An Account Under The Allowance Method Accountingcoach

The provision is a future loss - a future loss that must be recorded as soon as it. Provision for doubtful debts seems to be suffering from the same predicament beacuse strictly speaking the estimate for doubtful debts is not an obligation to an external party as per IAS 37 definition of a provision. The effects of provision for doubtful debts in financial statements may be summed up as follows. If Provision for Doubtful Debts is the name of the account used for recording the current periods expense associated with the losses from normal credit sales it will appear as an operating expense on the companys income statement. 100000 through following entry. A corresponding debit entry is recorded to account for the expense of the potential loss. Provision for Doubtful debts is an expense which occurs in the normal course of business. 200000 x 50 Rs. It may be included in the companys selling general and administrative expenses. When increase then expense deducted from profit and when decrease then income added in.

If Provision for Doubtful Debts is the name of the account used for recording the current periods expense associated with the losses from normal credit sales it will appear as an operating expense on the companys income statement.

Bad debts for the current year are to be set off and an additional amount of provision is to be added. Various organizations create a provision for all the future expected expenses and losses which may arise due to the credit sales so the organization needs to create a percentage of such provision on the net value of sundry debtor for complying with all the future uncertainties. 100000 through following entry. Under the accounting standard FRS 39 which sets out the principles for recognising and measuring financial instruments general and specific provisions for bad and doubtful debts will no longer be made. Provision for Doubtful Debts means the expense reported on the income statement or profit and loss Ac. The provision is used under accrual basis accounting so that an expense is recognized for probable bad debts as soon as invoices are.

If Provision for Doubtful Debts is the name of the account used for recording the current periods expense associated with the losses from normal credit sales it will appear as an operating expense on the companys income statement. The provision for doubtful debts is an accounts receivable contra account so it should always have a credit balance and is listed in the balance sheet directly below the accounts receivable line item. Bad debts for the current year are to be set off and an additional amount of provision is to be added. Provision for Doubtful Debts means the expense reported on the income statement or profit and loss Ac. It is an estimated matching of the cost of an asset over its useful life not an obligation to anyone. Under the accounting standard FRS 39 which sets out the principles for recognising and measuring financial instruments general and specific provisions for bad and doubtful debts will no longer be made. 100000 through following entry. 19 rows Provision for bad and doubtful debts general note impairment loss on trade debts. 200000 x 50 Rs. Management estimates that recovery of trade debts worth Rs.

If you want a full list of justifications. Every year the amount gets changed due to the provision made in the current year. It is identical to the allowance for doubtful accounts. 100000 through following entry. So it becomes bad debt at the same time as would any other line on your accounts receivable. It is an estimated matching of the cost of an asset over its useful life not an obligation to anyone. 19 rows Provision for bad and doubtful debts general note impairment loss on trade debts. The provision for doubtful debts or provision for bad debts is different to doubtful debts or bad debts. Bad debts for the current year are to be set off and an additional amount of provision is to be added. If Provision for Doubtful Debts is the current period expense associated with the losses from normal credit sales it will appear as an operating expense usually as part of Selling General and Administrative Expenses SGA.

A corresponding debit entry is recorded to account for the expense of the potential loss. Various organizations create a provision for all the future expected expenses and losses which may arise due to the credit sales so the organization needs to create a percentage of such provision on the net value of sundry debtor for complying with all the future uncertainties. It may be included in the companys selling. 200000 is doubtful and estimates a 50 chance of recovery in case of doubtful debts. 200000 x 50 Rs. Doubtful debts or bad debts is an expense and has already occurred. It may be included in the companys selling. If Provision for Doubtful Debts is the name of the account used for recording the current periods expense associated with the losses from normal credit sales it will appear as an operating expense on the companys income statement. The provision for doubtful debts is the estimated amount of bad debt that will arise from accounts receivable that have been issued but not yet collected. 100000 through following entry.

Various organizations create a provision for all the future expected expenses and losses which may arise due to the credit sales so the organization needs to create a percentage of such provision on the net value of sundry debtor for complying with all the future uncertainties. Provision for doubtful debts acts as a liability for the business and is shown on the liability side of a balance sheet. If Provision for Doubtful Debts is the name of the account used for recording the current periods expense associated with the losses from normal credit sales it will appear as an operating expense on the companys income statement. Under the accounting standard FRS 39 which sets out the principles for recognising and measuring financial instruments general and specific provisions for bad and doubtful debts will no longer be made. The two line items can be combined for reporting purposes to arrive at a net receivables figure. It may be included in the companys selling. The provision is a future loss - a future loss that must be recorded as soon as it becomes likely to. It may be included in the companys selling. According to ATO legislation this doesnt happen just because time has passed and its overdue but because you have tried your best to recover the debt and been unable to do so. Only change increase or decrease in provision for doubtful is shown in the income statement.

100000 through following entry. If Provision for Doubtful Debts is the current period expense associated with the losses from normal credit sales it will appear as an operating expense usually as part of Selling General and Administrative Expenses SGA. Allowance for doubtful debts is created by forming a credit balance which is netted off against the total receivables appearing in the balance sheet. The provision is a future loss - a future loss that must be recorded as soon as it. Only change increase or decrease in provision for doubtful is shown in the income statement. 200000 is doubtful and estimates a 50 chance of recovery in case of doubtful debts. It may be included in the companys selling. If Provision for Doubtful Debts is the name of the account used for recording the current periods expense associated with the losses from normal credit sales it will appear as an operating expense on the companys income statement. Bad debts for the current year are to be set off and an additional amount of provision is to be added. It may be included in the companys selling general and administrative expenses.