Fun Investment In Subsidiary Ifrs 9 Md&a Section Of 10k

Classification Of Financial Assets Liabilities Ifrs 9 Ifrscommunity Com

Investments in unit trusts or money market funds that themselves invest in a pool of debt and equity instruments. Inter-company financings that in substance form part of an entitys investment in a subsidiary are not in IFRS 9s scope. IFRS 9 responds to criticisms that IAS 39 is too complex inconsistent with the way entities manage their businesses and risks and defers the recognition of credit losses on loans and receivables until too late in the credit cycle. Ad Plus500SG - Trade CFDs with Tight Spreads and No Commissions. In respect of Question A the staff consider at initial recognition in IFRS 9414 refers to the date on which the entity begins to apply the requirements in IFRS 9 to its retained interest ie. Rather IAS 27 applies to such investments. Rather IAS 27 applies to such investments. Direct equity investments that do not meet the criteria to be accounted for as an subsidiary joint arrangement or associate and. When a parent ceases to be an investment entity the entity can account for an investment in a subsidiary at cost based on fair value at the date of change or status or in accordance with IFRS 9. When insufficient more recent information is available to measure fair.

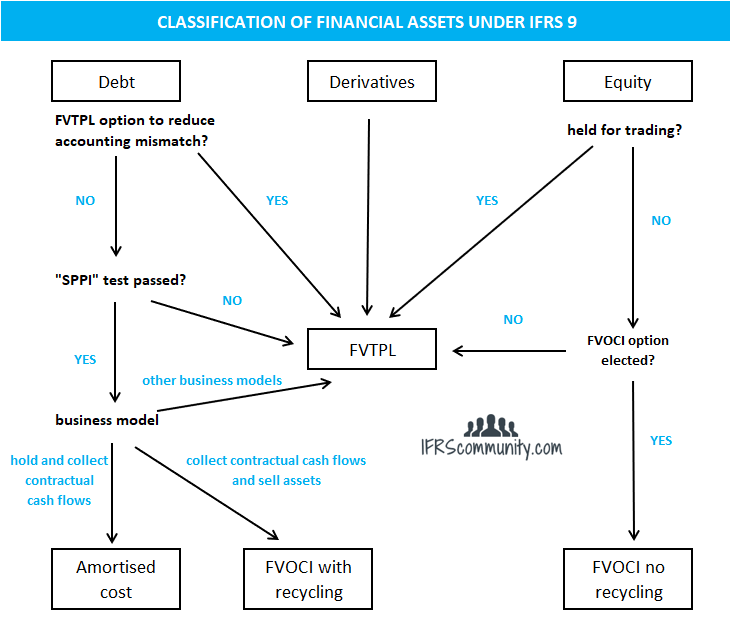

Accordingly IFRS 9 requires a company to measure simple debt investments at amortised cost when it holds those investments in order to collect their contractual cash flows.

Rather IAS 27 applies to such investments. IFRS 9 Financial Instruments defines the financial guarantee as a contract that requires the issuer to make specified payments to reimburse the holder for a loss it incurs because a specified debtor fails to make payments when due in accordance with the terms of a debt instrument. In respect of Question A the staff consider at initial recognition in IFRS 9414 refers to the date on which the entity begins to apply the requirements in IFRS 9 to its retained interest ie. This option as an amendment to IAS 27 is additional to the current two options available which allow entities to account for their investments in subsidiaries joint ventures and associates either at cost or in accordance with International Financial Reporting Standard IFRS 9 Financial Instruments IFRS 9 in their separate financial statements. In limited circumstances IFRS 9 permits an entity to use the cost as an appropriate estimate of the FV of unquoted equity investments. The holder of such an investment in a fund is required to apply IFRS 9 in its entirety to the investment unless the investment fund is a subsidiary associate or joint venture.

This option as an amendment to IAS 27 is additional to the current two options available which allow entities to account for their investments in subsidiaries joint ventures and associates either at cost or in accordance with International Financial Reporting Standard IFRS 9 Financial Instruments IFRS 9 in their separate financial statements. IFRS 9 generally is effective for years beginning on or after January 1 2018 with earlier adoption permitted. An inter-company loan is outside IFRS 9s scope and within IAS 27s scope only if it meets the definition of an equity instrument for the subsidiary for example it is a capital contribution. Direct equity investments that do not meet the criteria to be accounted for as an subsidiary joint arrangement or associate and. The investment funds financial statements and thus would be exempt from IFRS 9 apply IFRS 9 to its investment in the fund. This publication considers the changes to classification and measurement of financial assets. Part of the interest in the subsidiary associate or joint venture that is scoped out of IFRS 9. In limited circumstances IFRS 9 permits an entity to use the cost as an appropriate estimate of the FV of unquoted equity investments. In contrast if the company holds the same simple debt investment for sale then IFRS 9 requires the company to measure it at fair value with value changes recognised in PL. How will this change on adoption of IFRS 9.

Following the definition included in IFRS 9 applicable to financial assets not measured at fair value the closest analogy for investments in subsidiaries transaction costs should constitute only incremental costs that are directly attributable to the acquisition of the asset ie. Rather IAS 27 applies to such investments. In respect of Question A the staff consider at initial recognition in IFRS 9414 refers to the date on which the entity begins to apply the requirements in IFRS 9 to its retained interest ie. IFRS 9 will be effective for annual periods beginning on or after January 1 2018 subject to endorsement in certain territories. When a parent ceases to be an investment entity the entity can account for an investment in a subsidiary at cost based on fair value at the date of change or status or in accordance with IFRS 9. This option as an amendment to IAS 27 is additional to the current two options available which allow entities to account for their investments in subsidiaries joint ventures and associates either at cost or in accordance with International Financial Reporting Standard IFRS 9 Financial Instruments IFRS 9 in their separate financial statements. Part of the interest in the subsidiary associate or joint venture that is scoped out of IFRS 9. IFRS 9 requires equity investments except those accounted under the equity method of accounting or those related to a consolidated investee to be measured at FV. Further details on the new impairment model are included in In depth US2014-06 IFRS 9 - Expected credit losses. In contrast if the company holds the same simple debt investment for sale then IFRS 9 requires the company to measure it at fair value with value changes recognised in PL.

Inter-company financings that in substance form part of an entitys investment in a subsidiary are not in IFRS 9s scope. IFRS 9 responds to criticisms that IAS 39 is too complex inconsistent with the way entities manage their businesses and risks and defers the recognition of credit losses on loans and receivables until too late in the credit cycle. IFRS 9 will be effective for annual periods beginning on or after January 1 2018 subject to endorsement in certain territories. A capital contribution ie. In contrast if the company holds the same simple debt investment for sale then IFRS 9 requires the company to measure it at fair value with value changes recognised in PL. Part of the interest in the subsidiary associate or joint venture that is scoped out of IFRS 9. Costs that would not have been incurred if the entity had not acquired the asset. Further details on the new impairment model are included in In depth US2014-06 IFRS 9 - Expected credit losses. When insufficient more recent information is available to measure fair. How will this change on adoption of IFRS 9.

IFRS 9 requires equity investments except those accounted under the equity method of accounting or those related to a consolidated investee to be measured at FV. Inter-company financings that in substance form part of an entitys investment in a subsidiary are not in IFRS 9s scope. The date on which it loses control of the subsidiary and does not refer to the date it originally acquired the interest in the subsidiary. IFRS 9 generally is effective for years beginning on or after January 1 2018 with earlier adoption permitted. Following the definition included in IFRS 9 applicable to financial assets not measured at fair value the closest analogy for investments in subsidiaries transaction costs should constitute only incremental costs that are directly attributable to the acquisition of the asset ie. Further details on the new impairment model are included in In depth US2014-06 IFRS 9 - Expected credit losses. An inter-company loan is outside IFRS 9s scope and within IAS 27s scope only if it meets the definition of an equity instrument for the subsidiary for example it is a capital contribution. In limited circumstances IFRS 9 permits an entity to use the cost as an appropriate estimate of the FV of unquoted equity investments. Direct equity investments that do not meet the criteria to be accounted for as an subsidiary joint arrangement or associate and. The holder of such an investment in a fund is required to apply IFRS 9 in its entirety to the investment unless the investment fund is a subsidiary associate or joint venture.

The holder of such an investment in a fund is required to apply IFRS 9 in its entirety to the investment unless the investment fund is a subsidiary associate or joint venture. Accordingly IFRS 9 requires a company to measure simple debt investments at amortised cost when it holds those investments in order to collect their contractual cash flows. The investee is not an associate joint venture or subsidiary of the entity and accordingly the entity applies IFRS 9 Financial Instruments in accounting for its initial investment. IFRS 9 does NOT deal with your investments in subsidiaries associates and joint ventures look to IFRS 10 IAS 28 and related. How will this change on adoption of IFRS 9. Investments in unit trusts or money market funds that themselves invest in a pool of debt and equity instruments. You should recognize a financial asset or a financial liability in the statement of financial position when the entity becomes a party to the contractual provisions of the instrument please refer to IFRS 9 par. In respect of Question A the staff consider at initial recognition in IFRS 9414 refers to the date on which the entity begins to apply the requirements in IFRS 9 to its retained interest ie. When an entity becomes an investment entity it accounts for an investment in a subsidiary at fair value through profit or loss in accordance with IFRS 9. IFRS 9 generally is effective for years beginning on or after January 1 2018 with earlier adoption permitted.