Ifrs 17 Insurance Contracts Theactuary Net Actuarial Knowledge

The rationale behind this would be to limit the effect of volatility on Profit and Loss Accounts. According to the IASB IFRS 17 achieves this by. Of insurance contracts the effects IFRS 17 will have on a companys financial statements will vary from company to company even within the same jurisdiction4 Factors that will influence the effect that IFRS 17 will have on a companys financial statements include. The IFRS 17 balance sheet and income statement include. IFRS 17 is a complex standard and the interpretation of its requirements is subject to ongoing discussions. Investors and business managers use the income statement to determine the financial health of the. The objective of IFRS 17 is to ensure that an entity provides relevant information that faithfully represents those contracts. Given the above uses of current day gross written premium while insurers revise their recognition and recording of insurance contract revenue to comply with IFRS 17. Is an option to show financial impacts either in the Profit and Loss Account or Other Comprehensive Income. The main elements of the IFRS 17 standard address the reporting of earnings related to insurance contracts in the Statements of Financial Performance.

The main elements of the IFRS 17 standard address the reporting of earnings related to insurance contracts in the Statements of Financial Performance.

A the types and nature of the insurance contracts the company issues. IFRS 17 introduces a dramatically different approach to the definition and presentation of profit or loss and comprehensive income which is expected to have significant impact on the role of actuarial models in financial reporting. These illustrative IFRS financial statements are intended to be used as a source of general technical reference as they show suggested disclosures together with their sources. According to the IASB IFRS 17 achieves this by. The Illustration does not take into account any amendments to IFRS 17 that are proposed as a result of this process. IFRS 17 contains specific requirements regarding the reporting of revenue in the income statement and there are significant differences between the disclosures required under Solvency II and IFRS as discussed in the Presentation and disclosure section.

Other items of comprehensive income OCI do not flow through profit and loss. IFRS 17 Income Statement 9 9 PL 20X1 20X0 Insurance revenue 9856 8567 Insurance service expenses 9069 8489 Incurred claims and insurance contract expenses 7362 7012 Insurance contract acquisition costs 1259 1150 Gain or loss from reinsurance 448 327 Insurance service result 787 78 Investment income 9902 9030. These illustrative IFRS financial statements are intended to be used as a source of general technical reference as they show suggested disclosures together with their sources. IFRS 17 contains specific requirements regarding the reporting of revenue in the income statement and there are significant differences between the disclosures required under Solvency II and IFRS as discussed in the Presentation and disclosure section. The objective of IFRS 17 is to ensure that an entity provides relevant information that faithfully represents those contracts. Combining current measurement of future cash flows with the recognition of profit over the period that services are provided under the contract. The Illustration does not take into account any amendments to IFRS 17 that are proposed as a result of this process. The main elements of the IFRS 17 standard address the reporting of earnings related to insurance contracts in the Statements of Financial Performance. The rationale behind this would be to limit the effect of volatility on Profit and Loss Accounts. This guide illustrates one possible format for financial statements for an annual period beginning on 1 January 2023 when IFRS 17 and IFRS 9 Financial Instruments are applied for the first time.

According to the IASB IFRS 17 achieves this by. This information gives a basis for users of financial statements to assess the effect that insurance contracts have on the entitys financial position financial. IFRS 17 contains specific requirements regarding the reporting of revenue in the income statement and there are significant differences between the disclosures required under Solvency II and IFRS as discussed in the Presentation and disclosure section. A the types and nature of the insurance contracts the company issues. The rationale behind this would be to limit the effect of volatility on Profit and Loss Accounts. The IFRS 17 Income Statement and how this is affected by the Discount Rate Methodology For IFRS 17 reporting there is a completely new income statement which splits profits between insurance profits and investment profits. An income statement also known as profit and loss account is one of the financial statement that shows the income and expenses of a company for a specified time. These are illustrative IFRS financial statements of a listed company prepared in accordance with International Financial Reporting Standards. The objective of IFRS 17 is to ensure that an entity provides relevant information that faithfully represents those contracts. In October 2018 the IASB commenced a process of evaluating the need for making possible amendments to IFRS 17 to address certain reported concerns.

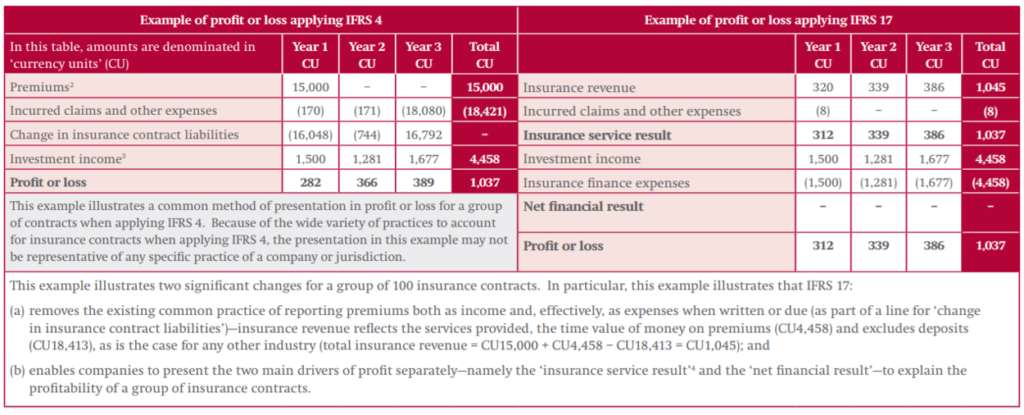

Profitability statement comparisons under IFRS 17 and IFRS 4. In October 2018 the IASB commenced a process of evaluating the need for making possible amendments to IFRS 17 to address certain reported concerns. The IFRS 17 balance sheet and income statement include. The objective of IFRS 17 is to ensure that an entity provides relevant information that faithfully represents those contracts. Of insurance contracts the effects IFRS 17 will have on a companys financial statements will vary from company to company even within the same jurisdiction4 Factors that will influence the effect that IFRS 17 will have on a companys financial statements include. Like US GAAP the income statement captures most but not all revenues income and expenses. This guide illustrates one possible format for financial statements for an annual period beginning on 1 January 2023 when IFRS 17 and IFRS 9 Financial Instruments are applied for the first time. These illustrative IFRS financial statements are intended to be used as a source of general technical reference as they show suggested disclosures together with their sources. According to the IASB IFRS 17 achieves this by. IFRS 17 Income Statement 9 9 PL 20X1 20X0 Insurance revenue 9856 8567 Insurance service expenses 9069 8489 Incurred claims and insurance contract expenses 7362 7012 Insurance contract acquisition costs 1259 1150 Gain or loss from reinsurance 448 327 Insurance service result 787 78 Investment income 9902 9030.

This information gives a basis for users of financial statements to assess the effect that insurance contracts have on the entitys financial position financial. This is different to the current IFRS 4 income statement where there is no such split. According to the IASB IFRS 17 achieves this by. This guide illustrates one possible format for financial statements for an annual period beginning on 1 January 2023 when IFRS 17 and IFRS 9 Financial Instruments are applied for the first time. A roll forward and analysis of movement of the CSM from one period to the next on historic assumption sets. A process to allocate new policies to a profitability group 3. A the types and nature of the insurance contracts the company issues. IFRS 17 is a complex standard and the interpretation of its requirements is subject to ongoing discussions. IFRS 17 introduces a dramatically different approach to the definition and presentation of profit or loss and comprehensive income which is expected to have significant impact on the role of actuarial models in financial reporting. Other items of comprehensive income OCI do not flow through profit and loss.

Presenting insurance service results including presentation of insurance revenue separately from insurance finance income or expenses. A roll forward and analysis of movement of the CSM from one period to the next on historic assumption sets. The objective of IFRS 17 is to ensure that an entity provides relevant information that faithfully represents those contracts. The Illustration does not take into account any amendments to IFRS 17 that are proposed as a result of this process. According to the IASB IFRS 17 achieves this by. Is an option to show financial impacts either in the Profit and Loss Account or Other Comprehensive Income. The new IFRS 17 disclosure in short. Categories IFRS 17 Insurance Contracts Tags Derecognition Bias Statement of Financial Position Probability Comparative information Financing activities Other comprehensive income Derivatives Financial guarantee contracts Contract modifications Time value of money The General Approach Asset or liability Financial performance Discount rate Insurance contract Embedded. This is different to the current IFRS 4 income statement where there is no such split. The IFRS 17 Income Statement and how this is affected by the Discount Rate Methodology For IFRS 17 reporting there is a completely new income statement which splits profits between insurance profits and investment profits.