Sensational Deferred Rent On Balance Sheet Toys R Us Financial Statements

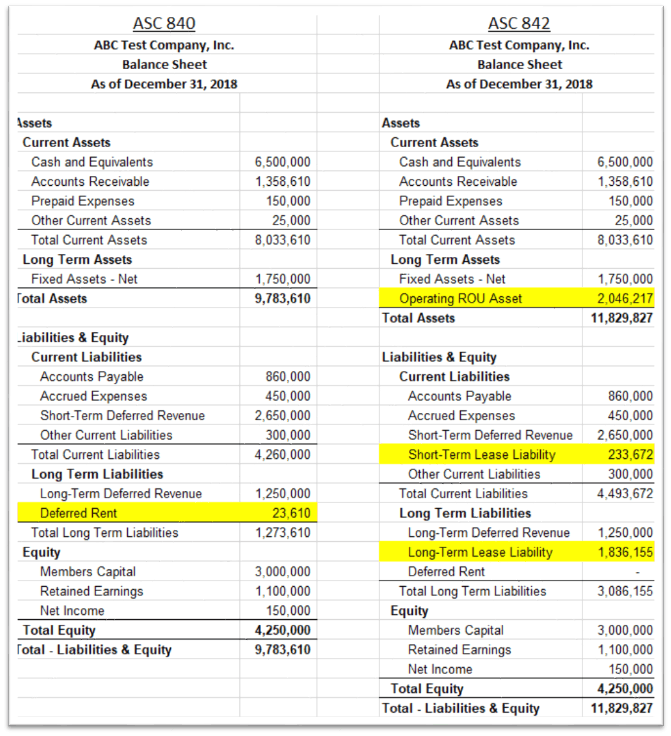

Asc 842 Summary Of Balance Sheet Changes For 2020

A balance will build up and then burn off when the cash paid exceeds the amount expensed. Deferred rent is a balance sheet account traditionally used in legacy accounting standards as defined in ASC 840. You continue this entry and by the time the lease is over your. Basically when cash paid for rent did not equal the average or straight-line rent required by ASC 840 the temporary difference was held on the balance sheet in the deferred rent account. A companys balance sheet reflects its assets and liabilities. The corporation can then match the assets cost with its long-term value. The difference between the straight-line expense and lease payments is accounted as deferred or prepaid rent under ASC 840. Deferred rent arises when the amount expensed exceeds the amount paid. To account for those differences the accountant should use a deferred rent expense account. Deferred rent is one of those liabilities but accountants generally total up the rent payments for the year subtracting the free months before dividing it all by 12.

Deferred rent accounting occurs when a tenant is given free rent in one or more periods usually at the beginning of a lease agreement.

To account for these free periods as well as subsequent periods the essential accounting is as follows. Compile the total cost of the lease for the entire lease. To account for those differences the accountant should use a deferred rent expense account. The transition to ASC 842 will result in the elimination of the deferred rent account from the balance sheet but will generally not impact net income or. Determine the cost of the lease for its entire period including free months discounted months or months that go up because of inflation. When deferred rent is calculated an accountant determines the rate of return also known as the gross rental income which is obtained from the balance sheet at the current market rents as well as any deferred rent payments that have been made on the property in the previous year.

Compile the total cost of the lease for the entire lease. While operating leases under ASC 840 are not recorded on the balance sheet as they are under ASC 842 rent abatements and escalations will have an effect on the deferred rent recognized in a period. The assets value decreases along with its depreciation amount on the companys balance sheet. The difference makes up the deferred portion of the rent. Deferred revenue is recognized as. When you make the monthly payments as per the lease agreement you must debit deferred rent and subsequently credit cash. To account for those differences the accountant should use a deferred rent expense account. Deferred rent is a liability created when the cash payments and straight-line rent expense for an operating lease under ASC 840 do not equal one another. Deferred rent is a balance sheet account that was used primarily in legacy lease accounting standards ASC 840 and IAS 17 however the concept still applies to the new ASC 842 standard but with very different presentation. Deferred rent is a balance sheet account traditionally used in legacy accounting standards as defined in ASC 840.

In this example each month for the first six months of the lease the deferred rent. The assets value decreases along with its depreciation amount on the companys balance sheet. Deferred rents are recorded in either an asset account eg other current or noncurrent assets when the cumulative difference between rent expenses and rent payments as of a balance sheet date is negative or a liability account eg other current or noncurrent liabilities when the cumulative difference is. Deferred rent is a balance sheet account traditionally used in legacy accounting standards as defined in ASC 840. Deferred rent is a liability created when the cash payments and straight-line rent expense for an operating lease under ASC 840 do not equal one another. To account for those differences the accountant should use a deferred rent expense account. Deferred rent was the primary mechanism used for straight-lining. Deferred rent accounting occurs when a tenant is given free rent in one or more periods usually at the beginning of a lease agreement. While operating leases under ASC 840 are not recorded on the balance sheet as they are under ASC 842 rent abatements and escalations will have an effect on the deferred rent recognized in a period. Companies accrue and report expenses in the period in which an expense is incurred to match with the revenue that the incurrence of the expense helps generate based on the expense matching principle of the accrual.

The difference makes up the deferred portion of the rent. Deferred rent is a balance sheet account traditionally used in legacy accounting standards as defined in ASC 840. In this example each month for the first six months of the lease the deferred rent. In order to deal with this situation the balance sheet must include a deferred rent asset or liability account. Deferred rent accounting occurs when a tenant is given free rent in one or more periods usually at the beginning of a lease agreement. Deferred rent is the balance sheet account that was used under ASC 840 to enable straight-line rent expense. When you make the monthly payments as per the lease agreement you must debit deferred rent and subsequently credit cash. Its amount in this journal entry can be calculated by using the total rent payment in the lease agreement dividing by the payment period. A balance will build up and then burn off when the cash paid exceeds the amount expensed. Deferred revenue is recognized as.

A companys balance sheet reflects its assets and liabilities. Deferred rent is a liability created when the cash payments and straight-line rent expense for an operating lease under ASC 840 do not equal one another. Deferred rent was the primary mechanism used for straight-lining. Determine the cost of the lease for its entire period including free months discounted months or months that go up because of inflation. The transition to ASC 842 will result in the elimination of the deferred rent account from the balance sheet but will generally not impact net income or. You continue this entry and by the time the lease is over your. The assets value decreases along with its depreciation amount on the companys balance sheet. The deferred rent account is a liability account on the balance sheet in which its normal balance is on the credit side. The difference makes up the deferred portion of the rent. A balance will build up and then burn off when the cash paid exceeds the amount expensed.

The transition to ASC 842 will result in the elimination of the deferred rent account from the balance sheet but will generally not impact net income or. Basically when cash paid for rent did not equal the average or straight-line rent required by ASC 840 the temporary difference was held on the balance sheet in the deferred rent account. Deferred rent is one of those liabilities but accountants generally total up the rent payments for the year subtracting the free months before dividing it all by 12. Deferred rent is a balance sheet account traditionally used in legacy accounting standards as defined in ASC 840. Deferred rents are recorded in either an asset account eg other current or noncurrent assets when the cumulative difference between rent expenses and rent payments as of a balance sheet date is negative or a liability account eg other current. Deferred rent arises when the amount expensed exceeds the amount paid. When deferred rent is calculated an accountant determines the rate of return also known as the gross rental income which is obtained from the balance sheet at the current market rents as well as any deferred rent payments that have been made on the property in the previous year. Determine the cost of the lease for its entire period including free months discounted months or months that go up because of inflation. 38 rows The deferred rents balance represents a deferred rent liability resulting from straight-lining. In this example each month for the first six months of the lease the deferred rent.